The first quarter of 2026 has given investors plenty to process. Global tariff uncertainty rumbles on, geopolitical tensions remain elevated, and local markets have had to absorb shifting interest rate expectations. Through it all, one reality hasn’t changed: the long-term case for disciplined, tax-efficient retirement investing is as strong as it has ever been.

Retirement annuities remain a cornerstone for long-term retirement investors: they enforce contribution discipline, offer powerful tax benefits, and channel capital into diversified balanced funds designed to ride out volatility. With fresh performance data to 31 March 2026, it’s the right moment to revisit which managers are actually delivering.

In this update, we reaffirm the role of RAs in building a bigger end-retirement pot and highlight the top-performing balanced funds over 3, 5 and 10 years — showing peer-group medians and fund counts for context. The goal: help you see which strategies are truly compounding so you can align your RA choices with your long-term retirement planning goals.

- Key Definitions

- Understanding the Aims of a Retirement Annuity

- How Retirement Annuities Work

- The Two-Pot Retirement System

- Investment Options for RAs

- Tax Benefits of a Retirement Annuity

- Accessing Your Retirement Annuity

- What Really Matters When Choosing an RA

- Best Performing Balanced Funds Over 3 Years

- Top Performing Balanced Funds Over 5 Years

- Best Performing Balanced Funds Over 10 Years

- Low-Cost Passive Balanced Funds

- Your RA on Death

- RAs vs. Offshore Investing

- Frequently Asked Questions

- Conclusion

Key Definitions

Retirement Annuity (RA)

A tax-efficient investment wrapper that holds your retirement savings until age 55. Contributions are tax-deductible, growth is tax-free, and assets fall outside your estate on death. Most RA assets are invested in Regulation 28-compliant balanced funds.

Regulation 28

The regulatory framework under the Pension Funds Act that governs how retirement funds may be invested. Currently permits up to 75% in equities and 45% offshore, with diversification requirements across asset classes.

ASISA Multi-Asset High Equity

The fund category used by ASISA (Association for Savings and Investment South Africa) for balanced funds that hold more than 60% in growth assets. This is the dominant category for Regulation 28-compliant balanced funds used inside RAs.

Two-Pot System

South Africa’s retirement reform implemented on 1 September 2024 that splits future contributions into a savings pot (one-third, accessible before retirement) and a retirement pot (two-thirds, preserved until age 55). Withdrawals from the savings pot are taxed at marginal income tax rates.

Total Investment Charge (TIC)

The all-in annual cost of holding a fund, including the management fee, performance fees, and other fund-level charges. A critical factor when comparing passive versus active fund options — lower TIC improves net compounding over time.

Understanding the Aims of a Retirement Annuity

A retirement annuity serves as a valuable tool to help you achieve financial security in your retirement years. It acts as an investment product that provides tax advantages, incentivising you to save for your future. The government encourages personal retirement savings to reduce dependence on state-funded support during old age.

If you belong to an employer-sponsored fund — such as a pension or provident fund — a retirement annuity can supplement your existing retirement savings. For those who are self-employed or not part of an employer fund, a retirement annuity can become your primary investment for retirement: a personal pension plan.

How Retirement Annuities Work

When you opt for a retirement annuity, you can make regular contributions or lump sum payments. You also have the freedom to choose how your retirement annuity funds are invested. Think of the retirement annuity as a protective “wrapper” that houses your investments. The type of wrapper determines the tax implications — different investment wrappers have varying tax consequences.

When you reach the minimum retirement age of 55, you can use the funds accumulated in your retirement annuity to invest in a post-retirement product. These products — such as living annuities or guaranteed life annuities — provide you with a regular income stream during your retirement years. Modern retirement annuities offer flexibility, allowing you to start or stop contributions based on your financial circumstances, such as periods of financial difficulty or job loss.

The Two-Pot Retirement System

South Africa’s two-pot retirement system, implemented on 1 September 2024, aims to balance long-term retirement savings with short-term financial flexibility. Under this system, retirement contributions are split into two components: a retirement pot, which remains preserved until retirement, and a savings pot, which allows limited withdrawals before retirement to help individuals access funds in times of genuine financial need.

While this offers greater liquidity, it also requires careful planning to avoid depleting future retirement savings. For a detailed breakdown of how the two-pot system works and what it means for your retirement planning, read our full article here.

Investment Options for RAs

All retirement annuities in South Africa are governed by Regulation 28 of the Pension Funds Act, which sets limits on asset allocation to ensure diversification and risk management. Under the current guidelines, retirement annuities can invest up to 75% in equities and 45% offshore — an increase from the previous 30% offshore limit. In addition to equities, RA portfolios can include bonds, property, hedge funds, and cash, allowing for a range of investment strategies.

Given these constraints, most retirement annuity assets in South Africa are allocated to balanced funds that comply with Regulation 28. These funds typically fall under the South African Multi-Asset High Equity ASISA category, making them the default choice for long-term retirement savers.

Tax Benefits of a Retirement Annuity

Retirement annuities offer several significant tax advantages. One structural benefit is that you cannot access the funds until you reach the minimum retirement age of 55, ensuring that your retirement savings remain on track.

Tax-Free Growth: The funds invested in a retirement annuity grow tax-free — you are exempt from income tax and capital gains tax on investment returns while the money remains in the fund.

Tax-Deductible Contributions: Contributions are tax-deductible up to a maximum of 27.5% of your gross income, capped at R430,000 per annum. This reduces your taxable income directly. For example: if you earn R1,000,000 per year and contribute R100,000 to an RA, your taxable income drops to R900,000 — reducing your tax bill by approximately R40,000 in that tax year. Any excess contributions above the annual cap are not lost; they are carried forward and can be deducted in future years or at retirement.

Estate Planning Benefit: All allowable contributions and accumulated growth fall outside your estate for estate duty purposes on death, which can represent a meaningful saving on larger portfolios.

Accessing Your Retirement Annuity

Once you reach age 55 or decide to retire, you can access the total value of your retirement annuity. You have the option to withdraw up to one-third of the total value as a lump sum. The first R550,000 of that cash withdrawal is tax-free — assuming you haven’t previously used any portion of this lifetime allowance. The remaining two-thirds must be used to purchase an income-producing product such as a living annuity or guaranteed life annuity.

A useful rule of thumb for sustainable income: a starting drawdown rate of around 4% p.a. For every R1,000,000 invested, that translates to approximately R40,000 per year before tax. If the total value of your retirement annuity is below R247,500, you may withdraw the entire amount as cash.

Note: The R550,000 tax-free lump sum threshold and R247,500 de minimis limit are subject to change — verify current figures at sars.gov.za before making any decisions.

What Really Matters When Choosing an RA

Determining the best retirement annuity depends on your specific needs and investment criteria. Key factors include fees, long-term performance, and the quality of underlying investments. While many investors focus on the platform or institution managing their RA — Old Mutual, Allan Gray, Glacier, Ninety One — what truly drives returns is the selection of funds within your RA. The platform is simply a vehicle; the investment strategy is what ultimately determines growth.

For most retirement annuities, balanced funds are the preferred choice, as they align with Regulation 28’s asset allocation limits. These funds typically target Inflation plus 5% per year — today roughly equivalent to a return of 10% p.a. and above. Achieving this benchmark is crucial, as it ensures investments grow in real terms, preserving and enhancing purchasing power in retirement. Not all balanced funds succeed in meeting this target, which makes fund selection a critical decision.

Interestingly, the top-performing balanced funds are often not managed by the biggest financial brands, but by boutique or specialist asset managers with a strong track record of consistent returns.

To help investors make informed choices, we’ve analysed Morningstar data as at 31 March 2026 to identify the best-performing balanced funds as potential options for your retirement annuity. All performance data is based on retail fee classes to ensure comparability.

Read More: In our article on the top retirement planning mistakes to avoid, we highlighted why looking outside the big brand names is so important.

Performance Context: Why Fund Selection Matters

With approximately 245 balanced funds in the market — 222 of which have at least a 3-year track record — this ASISA category offers more options than almost any other. Retirement savings represent the largest pool of investor capital in South Africa, which makes it a prime market for asset managers. But with so many options, not all funds deliver strong returns, reinforcing the importance of careful selection.

The performance gap between balanced funds remains significant. Over 3 years, the best-performing fund (Granate Balanced at 18.87% p.a.) and the worst-performing fund (Discovery Global Multi-Asset at 2.16% p.a.) sit 16 percentage points apart. That gap, compounded over a retirement savings horizon, translates into dramatically different outcomes.

For investors wanting to avoid the underperformers, we’ve also analysed the worst-performing balanced funds.

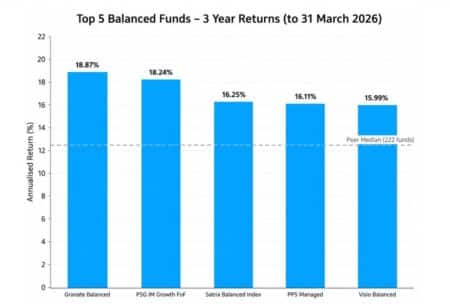

Best Performing Balanced Funds Over 3 Years

With 222 balanced funds in South Africa now boasting at least a 3-year track record (as at 31 March 2026), competition among managers remains fierce. The peer-group median return is 12.58% p.a., reflecting a broadly supportive backdrop for growth-oriented strategies. A select few have delivered exceptional outperformance, well above both the peer median and the typical Inflation-plus-5% target.

| Rank | Fund | 3-Year Return (ann.) |

|---|---|---|

| 1 | Granate Balanced | 18.87% |

| 2 | PSG Investment Management Growth FoF | 18.24% |

| 3 | Satrix Balanced Index | 16.25% |

| 4 | PPS Managed | 16.11% |

| 5 | Visio Balanced | 15.99% |

| Peer Group Median (222 funds) | 12.58% |

These funds have delivered outstanding returns through a highly eventful and unpredictable market cycle. For investors using retirement annuities as a long-term savings vehicle, choosing managers like these can materially improve the odds of meeting retirement goals. In the accumulation phase — where sequencing risk matters less — the priority is maximising growth within Regulation 28 constraints, accepting that volatility is the price of higher long-term returns.

Worth noting: the Satrix Balanced Index Fund, a passive strategy, has broken into the top three over three years, delivering 16.25% and comfortably beating the vast majority of actively managed peers. That result is worth reflecting on when evaluating the active versus passive debate.

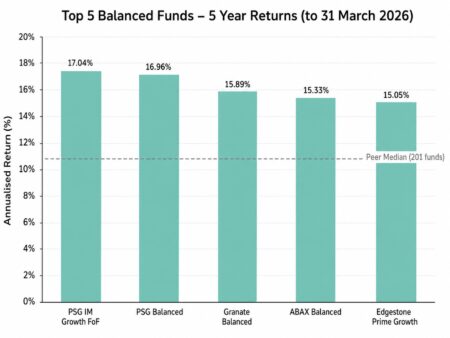

Top Performing Balanced Funds Over 5 Years

Across 201 balanced funds with a full 5-year record (as at 31 March 2026), the peer-group median sits at 10.82% p.a. The leaders below have shown durable, cycle-tested execution, compounding materially ahead of the median through differing market regimes.

| Rank | Fund | 5-Year Return (ann.) |

|---|---|---|

| 1 | PSG Investment Management Growth FoF | 17.04% |

| 2 | PSG Balanced | 16.96% |

| 3 | Granate Balanced | 15.89% |

| 4 | ABAX Balanced | 15.33% |

| 5 | Edgestone Prime Growth | 15.05% |

| Peer Group Median (201 funds) | 10.82% |

The PSG stable dominates the 5-year view, with both their Growth Fund of Funds and their flagship Balanced fund at the top of the table. These funds have compounded at roughly 15–17% p.a. over five years — well ahead of the peer group. The peer median of 10.82% p.a. also sits at or above the typical Inflation-plus-5% target, meaning the average balanced fund has broadly done its job over this period. For savers in the accumulation phase, that’s the kind of growth that builds the capital available at retirement.

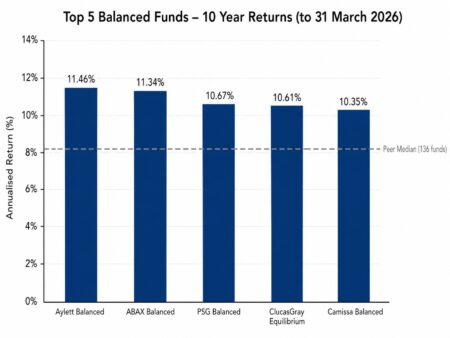

Best Performing Balanced Funds Over 10 Years

Long-term results tell the truest story. Among 136 balanced funds with a decade-long record (as at 31 March 2026), the peer-group median is 8.17% p.a. — a more sobering figure that falls short of the Inflation-plus-5% target most managers set for themselves. The standouts below have delivered sustained, long-run compounding well above the pack.

| Rank | Fund | 10-Year Return (ann.) |

|---|---|---|

| 1 | Aylett Balanced | 11.46% |

| 2 | ABAX Balanced | 11.34% |

| 3 | PSG Balanced | 10.67% |

| 4 | ClucasGray Equilibrium | 10.61% |

| 5 | Camissa Balanced | 10.35% |

| Peer Group Median (136 funds) | 8.17% |

Over a full decade, the standouts have shown real staying power. ABAX Balanced has been consistently among the top performers across all three time horizons, underscoring a durable investment process rather than a one-off style tailwind. Aylett Balanced posts the best 10-year record in the peer group, while PSG Balanced’s presence across both the 5-year and 10-year tables reinforces the value of a consistent, conviction-driven approach. Granate Balanced dominates the shorter-term tables but doesn’t yet have a full 10-year track record — one to watch as its history lengthens.

The 10-year peer-group median of 8.17% deserves attention. The average balanced fund has delivered roughly CPI plus 3% — meaningfully short of the CPI-plus-5% target most managers claim to pursue. That gap is a reminder that fund selection isn’t a marginal decision. Over a decade, the difference between the top performers (11%+) and the median (8%) compounds into a materially different retirement outcome.

Low-Cost Passive Balanced Funds

In recent years, low-cost balanced funds — passive or index-based strategies — have gained traction as viable alternatives to traditional actively managed options. Industry leaders such as Sygnia, Satrix, and 10X have been at the forefront of this shift, offering funds that rely primarily on indexation strategies rather than individual stock selection. While often labelled “passive,” these funds still involve active asset allocation decisions, particularly in balancing local and offshore exposure. The key advantage is cost efficiency, with Total Investment Charges (TIC) typically ranging between 0.50% and 0.70% p.a.

Within the main passive balanced cohort, five-year returns cluster around the broader peer median of 10.82% p.a. The table below compares each fund’s annualised 5-year return and peer-group rank across 203 qualifying funds.

| Rank (of 203) | Fund | 5-Year Return (ann.) |

|---|---|---|

| 18 | Satrix Balanced Index | 13.26% |

| 32 | Nedgroup Core Diversified | 12.24% |

| 61 | 10X Your Future | 11.58% |

| 64 | Sygnia Skeleton Balanced 70 | 11.54% |

| 79 | Prescient Balanced | 11.26% |

| 188 | Gryphon Prudential | 6.74% |

Universe context: Top fund ~17.04% p.a. | Top-decile cutoff ~12.72% p.a. | Median 10.82% p.a. | Bottom-decile cutoff ~7.63% p.a.

Among passive balanced options, the Satrix Balanced Index Fund is the clear standout over five years, landing in the top decile of the entire balanced universe. Nedgroup Core Diversified also sits firmly in the upper quartile. 10X Your Future, Sygnia Skeleton Balanced 70, and Prescient Balanced all cluster around the median — solid, steady outcomes broadly doing their job at lower cost.

Gryphon Prudential, by contrast, has materially lagged — ranked 188 of 203 with just 6.74% p.a. over five years. That’s barely ahead of cash and well below any reasonable real return target. The underperformance has been driven largely by sub-optimal asset allocation and elevated cash holdings — a stance that dampened compounding in a market that rewarded risk assets. It’s a useful reminder that “low cost” does not automatically mean “good outcome.” Asset allocation decisions still matter enormously, even inside a passive fund.

Your Retirement Annuity on Death

In the event of your passing, the value of your retirement annuity falls outside your estate, eliminating estate duty on those assets. The distribution of benefits is regulated by Section 37C of the Pension Funds Act. Trustees of the fund exercise their discretion to identify and arrange equitable payment to your dependants — both legal and factual — even if you have nominated a beneficiary. The definition of a dependant is broad, and the trustees have the final say, which can make the process complicated in practice.

Once the trustees have determined how benefits will be distributed, dependants can choose to receive the amount as cash (subject to taxation) or use the capital to purchase an income-generating product through a living or life annuity.

RAs vs. Offshore Investing: What’s the Right Balance?

A longstanding debate in financial planning is whether the tax benefits and incentives of a retirement annuity outweigh the potential advantages of offshore investing, which offers broader opportunities and hard currency returns.

The Rand has depreciated by an average of 5–6% per year over the last 30 years. For South Africans with global mobility aspirations — or who simply want to preserve purchasing power in real terms — that depreciation rate is a meaningful headwind that a predominantly rand-denominated RA can’t fully offset. Regulation 28’s 45% offshore limit helps, but may not be sufficient for investors with significant currency exposure concerns.

Ultimately, achieving financial security in retirement is about striking the right balance — leveraging the tax efficiency of an RA while ensuring enough offshore diversification to protect and grow wealth over time. The two are complementary, not competing.

Now Read: Offshore Investing and Top Offshore Investment Strategies for South African Investors

Frequently Asked Questions

What is the best retirement annuity in South Africa?

The best retirement annuity depends on the quality of balanced funds inside it, not the platform or brand name. Over 3 years to 31 March 2026, top performers include Granate Balanced (18.87% p.a.) and PSG Growth FoF (18.24% p.a.), well ahead of the 222-fund peer median of 12.58%. Selecting skilled managers with a consistent track record is the single most important decision.

How much can I contribute to a retirement annuity in South Africa?

You can deduct contributions up to 27.5% of your taxable income, capped at R430,000 per annum. This applies to combined contributions across all retirement funds — pension, provident, and retirement annuities. Any excess above the annual cap is carried forward and can be deducted in future years or at retirement.

Are passive balanced funds better than active funds for retirement annuities?

Not necessarily. While low-cost passive funds like the Satrix Balanced Index (rank 18 of 203 over 5 years) offer strong value, the best active managers have delivered materially higher returns — up to 17% p.a. over five years. The trade-off is between the certainty of low costs and the potential for outperformance through skilled active management.

What happens to my retirement annuity when I die?

Your retirement annuity falls outside your estate for estate duty purposes. Distribution is governed by Section 37C of the Pension Funds Act, where fund trustees allocate benefits to your dependants. While you can nominate beneficiaries, trustees retain discretion over the final allocation.

Can I withdraw from my retirement annuity before age 55?

Under the two-pot system introduced in September 2024, limited withdrawals from the savings pot (one-third of contributions) are possible before retirement. The retirement pot (two-thirds) remains preserved until age 55. Any early withdrawals are taxed at your marginal income tax rate, so the decision requires careful consideration.

A Balanced Approach to Retirement Investing

Retirement annuities remain a valuable tool in a well-structured retirement strategy, offering significant tax benefits and estate planning advantages. With a growing selection of low-cost options and top-performing boutique managers, they continue to be a solid foundation for long-term retirement savings.

But relying solely on a retirement annuity may not be enough to achieve true financial independence. Given Regulation 28 limits and long-term Rand depreciation, offshore investing should be a core component of a diversified retirement plan — not an afterthought. The two are complementary, and getting the balance right is what separates a good retirement plan from a great one.

The data is clear: fund selection matters, costs matter, and the gap between the best and the rest compounds significantly over time. A strong retirement plan isn’t about following conventional wisdom — it’s about making informed, strategic decisions that align with your long-term financial goals.

Further Reading: The Definitive Retirement Planning Guide for South Africans in 2026

If your retirement strategy is starting to feel like it needs a proper review — fund

selection, tax efficiency, offshore balance — we’re happy to have that conversation.

We work with professionals and business owners who are serious about getting the structure

right, not just the product. No commissions, no product incentives — just clear,

objective advice built around your situation.

This article is for informational purposes only and does not constitute financial advice. Henceforward (Pty) Limited is an authorised representative of Graviton Wealth Management (FSP 8772). Tax figures referenced are indicative — verify current rates and thresholds at sars.gov.za before making any decisions. Exchange control allowances are subject to SARB policy. Consult a qualified financial or tax advisor for advice specific to your circumstances.

Carl-Peter has been in the financial services industry since 2003 and launched Henceforward with Steven Hall in 2021. He focuses primarily on investment strategy and portfolio construction with a retirement planning lens. Henceforward is a fee-only, flat-fee firm — no commissions, no product incentives. CP holds the CFP® designation and understands how important planning for financial security is in today's uncertain world.