You’ve probably heard of the 10-year US Treasury. It pops up in headlines, investor updates, and economic forecasts. But here’s the thing: very few people—outside of finance circles—actually understand just how important it is.

Despite recent credit rating downgrades, the 10-year Treasury remains the most influential risk-free interest rate in the world. It’s the foundation stone upon which global asset prices are built. And whether you’re a professional portfolio manager or someone just trying to grow your retirement pot, this is a number you need to know.

Even if you live in Cape Town or JHB, invest in rand-based funds, or are mostly focused on local goals, the 10-year Treasury quietly shapes your investment outcomes in the background. Think of it like gravity in the financial universe—always there, always pulling, even if you’re not watching.

Let’s break it down.

Think of the US government as the most creditworthy borrower on the planet. When it wants to raise money, it issues IOUs—called Treasury bonds. The 10-year version is the one investors watch most closely. It pays a fixed interest rate for 10 years and returns your capital at the end.

Because it’s backed by the “full faith and credit” of the United States government, the 10-year Treasury is considered virtually risk-free—meaning there’s almost no chance you won’t get your money back. In investment speak, it’s the global benchmark for what “safe” looks like

If investing is about weighing risks and rewards, then the 10-year Treasury gives us the baseline. What return should you get if you’re taking no risk? That’s the yield on the 10-year.

Every other financial instrument—from Eskom bonds to Apple shares—is priced off this so-called “risk-free rate.” Want to know if a stock is expensive? You compare its expected return to the 10-year yield. Want to issue corporate debt? You pay a premium above it. Want to evaluate your retirement fund’s long-term return assumptions? You’re probably anchored to it, even if indirectly.

Yes—even in South Africa.

Fund managers here use it when building diversified portfolios. Actuaries factor it into pension models. Asset allocators adjust their strategies based on where the yield is heading. So while the bond is issued in Washington, its ripple effects stretch right into Claremont, Sandton, and Stellenbosch.

Now, here’s a key reason the 10-year US Treasury holds its special status: credit ratings.

Credit rating agencies like Moody’s, S&P, and Fitch assess how likely a country—or company—is to repay its debt. The US, despite its enormous debt pile, still holds a very high credit rating. Though in a sign of the times, Moody’s recently became the last of the three major agencies to downgrade US debt, dropping it from AAA to AA+.

Even with this downgrade, the US remains one of the most trusted borrowers globally.

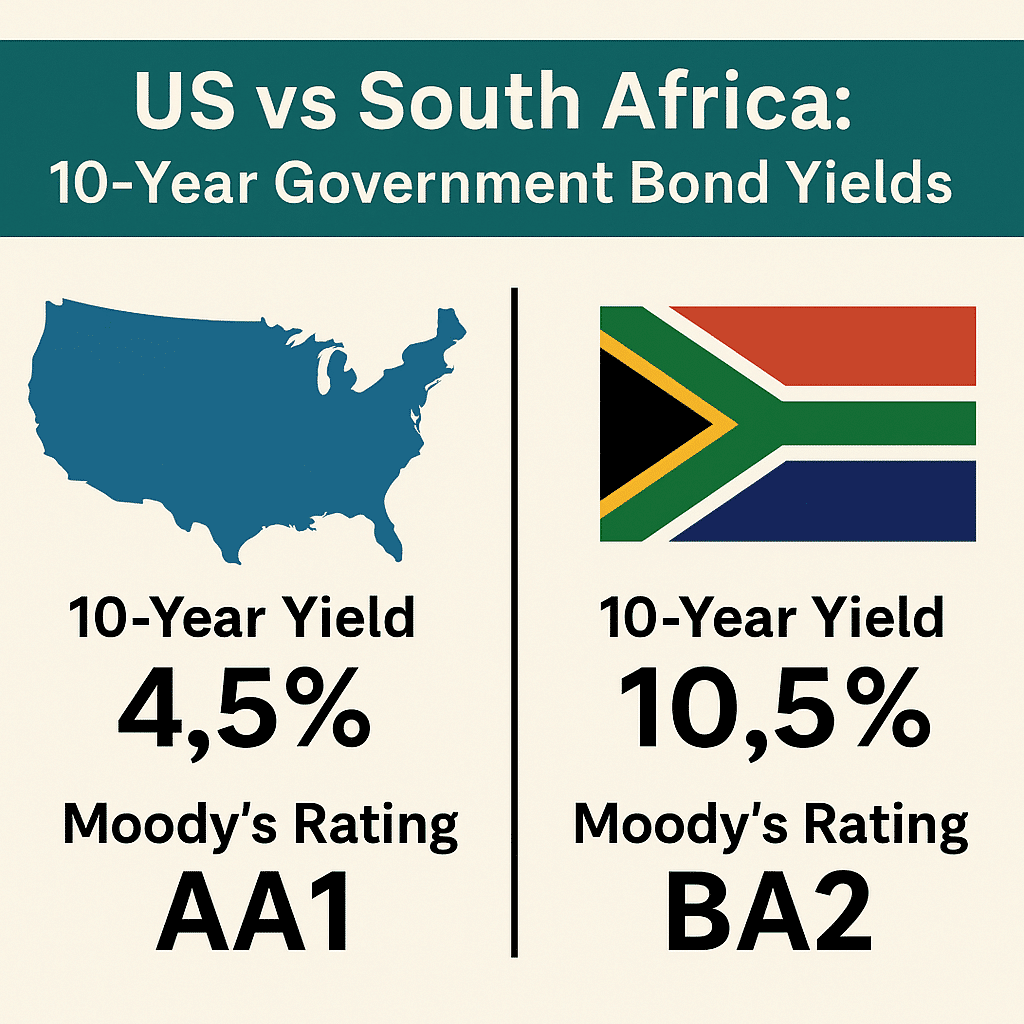

South Africa, by contrast, has been sitting in “junk status” since 2020, with ratings several notches below investment grade. That means global investors perceive higher risk, whether due to weak fiscal discipline, low growth, or political noise.

So, the difference in yields isn’t arbitrary (as at 26 May 2025).

There are a handful of countries that still boast pristine credit ratings from all three agencies. These include Germany, Switzerland, Singapore, and a few others with strong fiscal positions and political stability.

Interestingly, the divergence in yields between the US and some of these AAA-rated countries began to widen noticeably around 2011, when the US lost its AAA-rating from S&P for the first time. Since then, the US has typically offered higher yields than countries like Germany, not necessarily because it is riskier in a practical sense, but because the market demands a slightly higher return for what is no longer rated “perfect.”

This yield premium, though small, reflects that even the global benchmark is not immune to scrutiny.

Here’s where the plot thickens: the 10-year Treasury doesn’t just sit in a vacuum—it’s the anchor for global borrowing costs.

If the yield rises, so do mortgage rates, vehicle finance costs, and credit card rates. That’s true in the US, but also in Europe, Asia, and yes—South Africa.

SA government bond yields often move in tandem with US Treasuries. When the 10-year jumps, global investors reprice everything else higher too. That means South African borrowers—including our own government—may have to pay more to attract capital.

Bond prices and yields move in opposite directions. When demand for the bond goes up, the yield falls. When investors start selling, the yield rises.

So when you hear that the 10-year yield has “spiked,” it might mean inflation is back, the US Federal Reserve is hiking rates, or markets are nervous about government debt levels. When yields fall, it can mean a recession is looming and investors are seeking safety.

There’s also the yield curve—a fancy term for how different bond maturities stack up. If short-term yields rise above long-term ones (an “inverted yield curve”), that’s often a warning sign for a recession.

Further Reading: Understand the different forms of investment risk and how that applies to various asset classes

If you’ve ever wondered why the rand suddenly weakened, or why your offshore fund took a knock even though you invested in “safe” US bonds—chances are, the 10-year Treasury yield played a role.

Here’s how it connects to your world:

1. The Rand: Higher US yields often lead to a stronger dollar, which can put pressure on emerging market currencies like the rand.

2. Capital flows: Global investors may pull money out of South African bonds and equities in favour of US Treasuries if the yields are more attractive.

3. Offshore investing: If you own global unit trusts, ETFs, or retirement products with foreign exposure, those portfolios are impacted by shifts in this rate.

4. Pension projections: Long-term modelling by retirement funds and investment houses often uses the 10-year as a core assumption.

In short: the 10-year Treasury might not headline your financial plan, but it definitely plays a supporting role

Globally, government bonds—especially US Treasuries—are used to reduce volatility in portfolios, acting as a buffer when equities fall. In South Africa, however, government bonds often play a dual role: they provide high levels of income and have historically offered strong capital growth, particularly during periods of falling inflation or interest rates.

So, while bonds are sometimes seen as the “boring” part of a portfolio, in reality they’re doing some heavy lifting—whether it’s stabilising returns or delivering income. And understanding how the 10-year US Treasury behaves gives you a better sense of how the bond portion of your portfolio might respond in different market conditions.

Further Reading: Timeless principles for achieving long-term investment success

Over the past few years, the 10-year yield has been on a rollercoaster. In 2020, it plunged below 1% during the pandemic panic. By 2022, it surged past 4% as inflation came roaring back and the US Federal Reserve hiked rates aggressively.

Lately, volatility has remained elevated not just due to inflation and monetary policy, but also because of rising concerns around US fiscal sustainability. With debt-to-GDP ratios at historic highs, regular debt ceiling standoffs, and persistently high deficits, investors are increasingly questioning how much more the US can borrow before the market demands a higher yield to absorb the risk.

This growing scrutiny has led to sharper and more unpredictable moves in the 10-year yield, as market participants digest mixed signals from the Fed, political developments in Washington, and global shifts in capital flows.

When bond yields rise, bond prices fall—and vice versa. The longer the maturity of the bond, the more sensitive it is to changes in interest rates. This is known as duration risk.

As a rule of thumb, a 10-year bond has a duration of around 8 to 9 years. So, if the 10-year yield rises by 1%, the price of the bond could drop by 8–9%. Likewise, if yields fall by 1%, the bond’s price could rise by a similar percentage.

That’s why yield moves matter—not just for future returns, but for the value of bond portfolios right now.

Over the past few years, the 10-year yield has been on a rollercoaster. In 2020, it plunged below 1% during the pandemic panic. By 2022, it surged past 4% as inflation came roaring back and the US Federal Reserve hiked rates aggressively.

Every jump in yield created waves in stock markets, property funds, cryptocurrencies—you name it. Investors learned (sometimes the hard way) that when the risk-free rate changes, so does the value of everything else.

Further Reading: What are Secular Bear Markets and Could We Be Heading for One?

You don’t need to be a bond trader to care about the 10-year Treasury. But as an investor—or just someone planning your financial future—you should know the basics.

It helps you understand why markets are moving. It adds context to your investment returns. And it reminds you that, like it or not, we’re all swimming in the same global financial ocean.

Want to check the yield? Just Google “10-year Treasury yield” or look it up on Bloomberg or CNBC. It won’t tell you everything—but it’ll tell you more than most headlines.

Carl-Peter Lehmann is a CERTIFIED FINANCIAL PLANNER® and Director at Henceforward, a South African wealth management firm that helps clients navigate complex financial decisions with clarity and confidence. He specialises in retirement and investment planning, with a particular focus on offshore strategies and personalised advice for high-net-worth individuals.